This is the fourth edition of our monthly snapshot (most recent versions here and here). This is our July version of the same report, analyzing consumer activity across more than 1.5MM online product pages from more than 1,200 retail/brand sites.

This time, we focused on a four-month period (starting February 24, 2020 and ending June 28, 2020). In each report, we specifically analyze review submission levels, review length and sentiment, overall conversions/sales volumes, and review consumption (both absolute and among those who go onto purchase).

We are seeing stabilization in most of the data we capture, as the market seemingly adapts to a new “normal”. But let’s dig deeper into the specifics of what this actually means.

Key ecommerce market trends

01

02

03

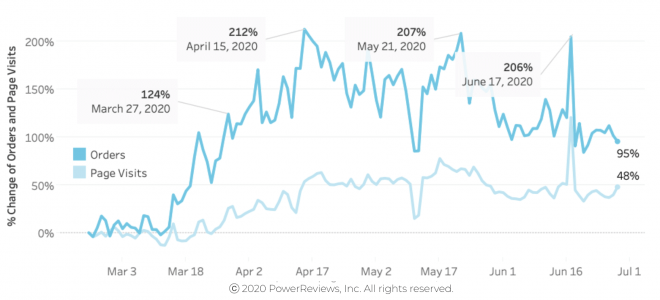

Both online order and traffic volumes flatten out to a (revised) “new normal”?

Over the past three months, we have reported aggressive growth in ecommerce purchase volumes since we started measuring at the back end of February. We speculated then that we had hit a potential “new normal” with highs of a 3x increase between that end of February date consistent across both April and May. We also pondered the impact of “Stay at Home” orders being lifted, as was the case in some states in June.

Throughout June, this certainly had an affect. We saw fluctuating demand during the month, with highs (of 206% above end of February levels) consistent with April and May. But, for the most part, we saw lower order volumes than we did in those two months. On our last date for capturing this data (June 28th), order volumes fell to around double (+95%) what they were pre-pandemic. They were approximately at this level throughout June, indicating that reopening was definitely having an impact. COVID-19 has clearly driven consumers online and so it’ll be very interesting to see if this sticks longer term.

Traffic has increased steadily over the past four months and hasn’t shown any sign of falling recently, which demonstrates a clear shift in consumer behavior. Customers are now far more comfortable shopping online but have become less decisive – perhaps due to broader economic uncertainty, job insecurity and associated pressures.

Both traffic and purchase volumes stabilize in June

Review submission levels fall slightly, but still significantly above pre-pandemic norms

In last month’s snapshot, we reported a giant 2.3x leap in review submission levels from April to May. After this big increase, volumes dropped in June – peaking at 54% above pre-pandemic levels on June 15 (consistent with the high in April). This is to be expected to a certain extent given the drop off in purchase volumes reported above.

However, it’s important to note that review submission volumes are still way above what we saw pre-pandemic. This is despite an initial drop off throughout March, when review submission actually dropped right at the time “Stay at Home” orders kicked in.

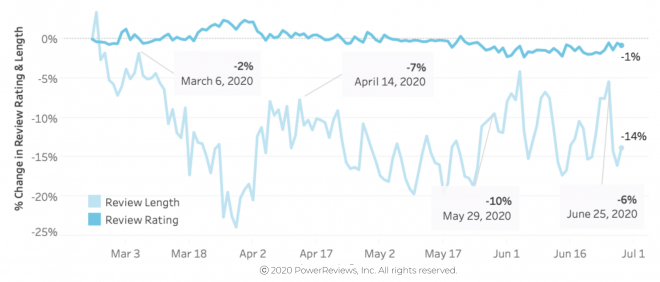

In terms of the actual content of reviews, there were not any huge shifts. Sentiment – in the form of average rating – remains flat, which makes sense given the products themselves are unlikely to have changed significantly in this period. Review length is down slightly on pre-pandemic levels but, given the average review length is 154 characters, a decrease of 10-20% is not particularly significant or meaningful. In last month’s webinar, we focused on review length in detail and offered some tips how to improve review quality. Check out our blog for a summary of that webinar.

Review submission volumes fall slightly in May but up on “normal”

Review length and ratings stable through June

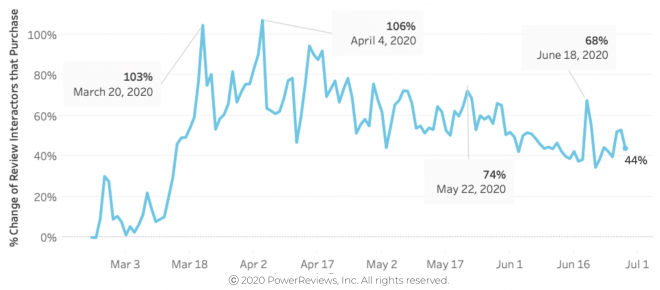

Review content continues to be critical to driving purchase decisions

Review content continues to be more influential on the path to purchase than it was before the pandemic. The June high of our review interaction measure (the extent that consumers who convert engage with review content i.e. sorting, filtering, etc.) proved consistent with what we saw in May at 74% and 68% above pre-pandemic levels respectively. Overall review engagement is up around 1.5x on “normal” times.

With that being said, this has dropped since February and March. There are most likely two reasons for this: 1. Purchase volumes have also fallen in this period and 2. The initial surge was likely due to consumers flooding online, buying products they previously had never bought before, and searching for validation before purchasing.

Bottom line: Shoppers are still heavily relying on review content to assess product quality and make purchase decisions.

Reviews continue to influence purchase at a higher rate than pre-pandemic

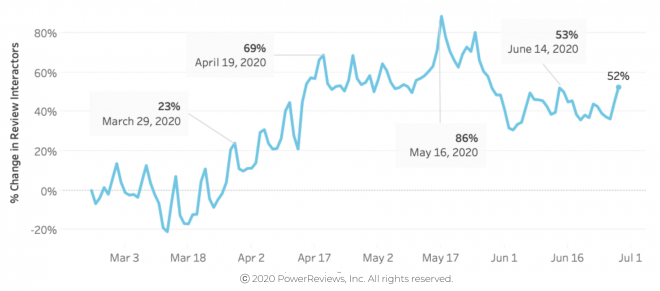

Review engagement stable at around 1.5x pre-pandemic

Summary

The re-opening of a number of states led to month-over-month decreases in most of the metrics we capture: purchase levels, review submissions, and review interaction volumes.

However, these are still way above comparative figures from when we started our research pre-pandemic at the end of February.

Specifically, purchase levels are double what they were pre-pandemic (purchase levels had tripled in May and April). Review interaction volumes have consistently increased, and are up between 50% to 65% during this time period. This is indicative of consumers seeking out greater social proof as they shop for products they are not as familiar with.

Review submission levels are also up from where they were pre-pandemic but have slightly fallen off lately. This is to be expected given the reduction in overall sales volumes.

Given the tightening of restrictions in many states that reopened earlier and the rapid change in consumer behavior more generally, we would expect increases across the board during July.